Gay Cororaton, Chief Economist

The median rent paid for new leases continued to cool in May 2023 but Miami’s rent growth is still outpacing the nation as the city continues to experience sustained migration, job creation, and continued recovery of tourism and travel.

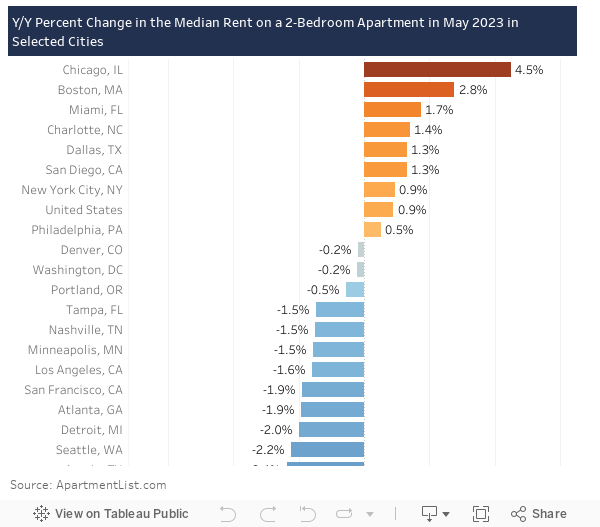

Nationally, the median rent on a 2-bedroom apartment rose 0.9% from one year ago, according to ApartmentList.com, an apartment listing site. In the city of Miami, the median rent paid for new leases on a 2-bedroom unit rose 1.7%.

Among selected 25 major cities, Miami ranked third in rent growth and one of nine cities with an annual rent growth. In contrast, many Sunbelt markets experienced slower rent increases or rent declines such as Dallas, Tampa, Atlanta, Austin, Nashville, Las Vegas, and Phoenix, where multifamily rental vacancy rates were higher in some markets compared to the Miami metro area.

Among the South Florida cities, the median rent on new leases of 2-bedroom apartments rose over 2% in Hialeah (6.7%), Coral Springs (3.8%), Lauderhill (2.0%), and North Miami Beach (2.0%), with demand seeming to come from a mixed group of renters with diverse needs that cater to their income affordability, amenity desires, or lifestyle needs.

The modest rent growth is a healthier pace than the torrid double-digit growth in 2020-2021 that hit as high as 18% in November 2021.

Rent Growth Cools as More Rental Listings Hit the Market

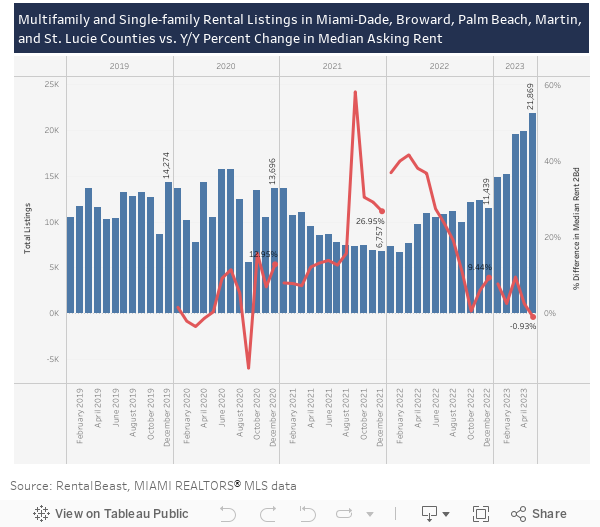

Rent growth started to cool in the second half of 2022 as more listings hit the market. Total listings of multifamily and single-family homes rose to 22,872 in May 2023, about thrice the 7,056 listings in January 2022, according to RentalBeast®1 and MIAMI Realtors® MLS rental listings data.

The share of single-family rentals sharply rose in 2022 to 29.1% (24.2% in 2021) and further increased to 33.8% of the listings from January through May 2023. There were 7,418 single-family homes listed for rent in May 2023, up from 2,062 in January 2022.

The rise in single-family rentals could be due to both demand and supply factors. On the demand side, this could be due to the rise of hybrid or fully remote work. Single-family homes provide more workspace. A hybrid work schedule also enables workers to live further away in the suburbs where single-family homes are more prevalent because of the reduced commute.

On the supply side, one plausible reason is that some homeowners are choosing to rent rather than sell their home when moving to another home due to the high rent growth in the past two years and the desire to keep the home equity gains. For example, in Miami-Dade, the median asking rent on a single-family home has risen nearly 80% as of May 2023 since May 2019, while the median single-family existing home sales price has increased by 69% to $600,000 as of April 2023 compared to the pre-pandemic level in April 2019.

Another source of supply of single-family homes for rent are investors and single-family built-for-rent housing.

According to Redfin, a national real estate brokerage, the share of investor purchases to total home sales in the Miami metro area rose from 20% in 2020 Q3 to 30% in 2023 Q12.

In the South region, U.S. Census Bureau data on housing starts by purpose and design indicates that single-family homes built-for-rent accounted for 7.6% of total housing starts in 2022 (21,000 homes out of 581,000), up from just 4.5% in 2019 (17,000 homes out of 497,000 units). In addition, single-family homes built as condos (non-fee simple) can be used for rental purposes, with this share averaging 4% over recent quarters nationally, according to the National Association of Home Builders3.

Strong Multifamily Rental Demand Outlook But Financing Challenges Could Constrain New Construction

The outlook for rental demand in South Florida is fundamentally strong, buoyed by sustained migration, job creation, and continued recovery of tourism and travel.

However, the higher cost of borrowing and the pullback in financing in the wake of the two regional bank failures in March could hamper future construction and supply.

Commercial and industrial loans held by all commercial banks have declined to $2.8 trillion as of May 24, down 2.5% compared to the level on March 15. C&I loans are short-term loans to finance working capital needs like equipment purchases.

This pullback could further tighten the supply of new for-sale or for-rent housing in 2023-2024. The imbalance between the demand and supply of housing appears to be greatest in Broward where employment is rising at a much faster pace than housing permits, with 13 newly employed people in the past 12 months for every 1 housing permit issued in 2022.

On the positive side, tighter supply will keep the vacancy rate hovering at around 7% and support a modest expansion in rent growth.