By Gay Cororaton, Chief Economist

South Florida’s housing supply remains broadly tight compared to pre-pandemic level, supporting sustained price appreciation in this market. As of March 2023, 87% of 92 incorporated municipalities in Miami-Dade, Broward, and Palm Beach (where months’ supply data) have lower months’ supply of homes for sale compared to the levels in March 2019.[1]

Moreover, in 69 out of 91 municipalities, or 76% of market areas, the level of inventory is equivalent to less than 6 months’ supply. Supply conditions are extremely tight for homes priced at below $600,000, with active listings equivalent to about 2 months’ supply.

With tight supply, single-family home prices have appreciated in 75% of 88 incorporated municipalities in Miami-Dade, Broward, and Palm Beach (where price data is available) with the median single-family home sales prices higher from one year ago at the single-digit pace (Miami-Dade, 5.6%; Broward, 3.7%; Palm Beach, 6.3%).

Supply conditions are likely to remain tight in 2023, with new listings coming in at a pace just slightly above monthly absorption, at 11 new listings per ten new pending sales as of March 2023. As such, I expect South Florida’s median single-family home prices to broadly continue rising at a single-digit pace in 2023. Supply conditions are more likely to improve in 2024 as interest rates stabilize and with more new home construction coming into the market.

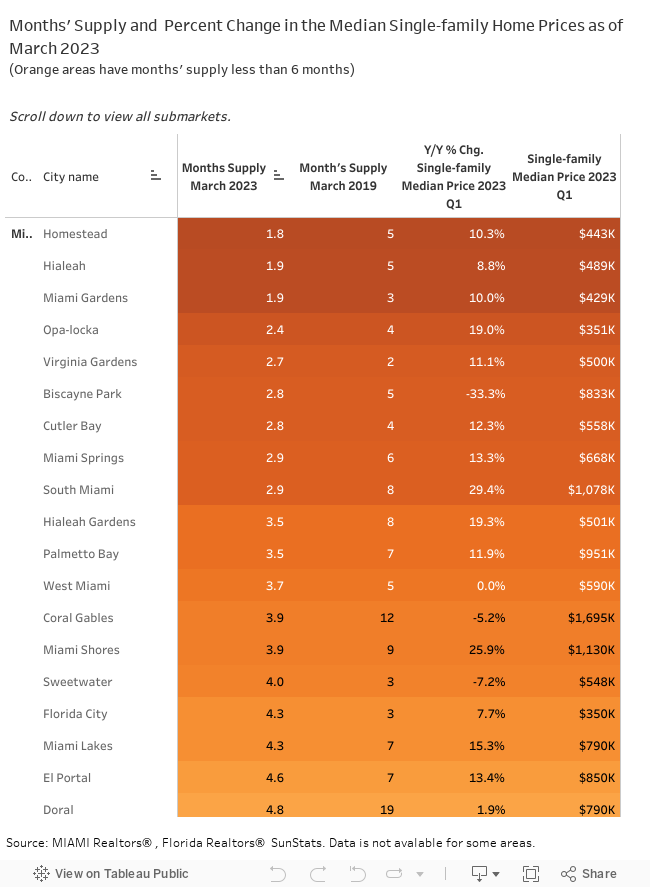

Miami-Dade County: 84% of municipalities have tighter supply than in 2019

In Miami-Dade County, 27 or 84% of 32 incorporated municipalities with available data had lower months’ supply of single-family homes in March 2023 than in March 2019. The lowest levels of months’ supply were in Homestead (1.8), Hialeah (1.9) and Miami Gardens (1.9) where the median single-family sales prices were below $500,000.

This tight supply has supported the price growth in 25 of the 32 Miami-Dade municipalities. The median single-family sales price during 2023 Q1 increased at double-digit rates in the low-price tier markets such as Hialeah Gardens (19.3%), Opa-Locka (19%), Miami Gardens (10%), Cutler Bay (12.3%), Homestead (10.3%), and Florida City (7.7%).

Prices also rose in mid-price tier markets nearer to the city of Miami such as Miami Lakes (15.3%) , Miami Springs (13.3%), and El Portal (13.4%), indicating a strong demand for homes closer to the city of Miami.

Single-family home prices declined in the upper price tier market of Coral Gables (-5.2%) as well as small luxury markets (fewer than 10 sales per quarter) although the price changes over time need to be taken with caution because property characteristics vary widely among luxury homes: North Bay Village (-2.2%), Key Biscayne (-2.2%), Bay Harbor Islands (-2.6%), and Sunny Isles (-40%).

In other luxury markets, single-family home prices were up year-over-year: Surfside (105%) , Bal Harbour (62%), Miami Beach (35%), and Aventura (25%). In luxury markets, 12 to 24 months’ supply is not unusual and such levels do not indicate a highly weak market.

Broward County: 97% of municipalities have tighter supply than in 2019

Housing supply is even tighter in Broward County where 29 out of 30 or 97% of incorporated municipalities with available data had lower months’ supply of single-family homes in March 2023 than in March 2019. The lowest levels of months’ supply were in Margate (1.4), North Lauderdale (1.6), and Tamarac (1.7) where the median single-family home sales prices hovered at $400,000, and in Coconut Creek (1.7) where the median single-family sales price was a little over $500,000.

Home prices rose at double-digit pace in low-price tier markets with median sales price of below $400,000 like Tamarac (21.3%), Lauderhill (11.6%), West Park (10.8%), and Lauder Lakes (10.8%).

On the other hand, home prices typically fell in the mid-price tier markets of Fort Lauderdale (-13.2%), Lauderdale-by-the-Sea (-9.5%) where month’s supply hovered at 5 to 6 months. However, the median sales price rose in the price tier markets of Lighthouse Point (13.6%) and Southwest Ranches (10.4%), but there are few transactions in these markets and the property characteristics and size vary widely so price comparisons need to be viewed with a grain of salt.

Palm Beach County: 83% of municipalities have tighter supply than in 2019

In Miami-Dade County, 24 or 83% of 29 incorporated municipalities with available data had lower months’ supply of single-family homes in March 2023 than in March 2019. The lowest levels of months’ supply were in Greenacres (1.0), Lantana (1.1) and Palm Springs (1.1) where the median single-family sales prices are below $400,000.

In Lantana and Haverhill, tight supply pushed the median sales prices to increase by 30% in 2023 Q1 from one year ago.

Jupiter and Tequesta, which are expensive markets with a median sales price in the $800,000 to $900,000 price range, saw slight price declines as the level of inventory started to accumulate from 1 months’ supply one year ago to 3 months’ supply as of March 2023, with active listings doubling from one year ago.

Housing Supply Outlook to Remain Tight with New Listings on Pace with Pending Sales

Supply conditions are likely to remain tight, as the pace of new listings is just matching the pace of monthly absorption, with an average of eleven new listings per 10 new pending sales as of March 2023 across Miami-Dade, Broward, Palm Beach, and Martin. This is slightly less than the ratio of twelve new listings per ten new pending sales in March 2019. As such, I expect South Florida’s median single-family home prices to broadly continue rising at a single-digit pace in 2023.

Since there are trade-up or trade-down buyers, higher mortgage rates could be disincentivizing moving during this time when mortgage rates are still rising. However, the lock-in effect is less problematic for the South Florida market than nationally because it has a higher share of cash sales than nationally (US, 27%; Miami-Dade, 40%, Broward, 41%, Palm Beach, 52%; Martin, 55% as of March 2023).

See Tableau data visualization below to view the data for this analysis.

[1] Where housing data is available from the Multiple Listing Service and compiled by Florida Realtors® and released on SunStats.